TL;DR: NFP mergers are accelerating across the UK, Australia, and New Zealand, but each country faces different pressures. UK charities merge out of financial desperation (94 mergers in 2024-25, up 49%). Australia’s sector appears strong (£489 billion in assets) but small charities struggle as costs outpace revenue. New Zealand sits between both, with organisations hesitant to consolidate despite mounting pressures. The lesson: merge from strength before crisis removes your options.

Core findings:

UK charity mergers hit record levels in 2024-25 (94 mergers, up 49% from previous year), driven by financial survival rather than strategy

-

60% of Australian charities operate on less than £500,000, with costs growing faster than income

-

New Zealand NFPs face similar pressures but cultural resistance to consolidation delays necessary decisions

-

Organisations that wait until crisis hits get worse merger outcomes and lose negotiating power

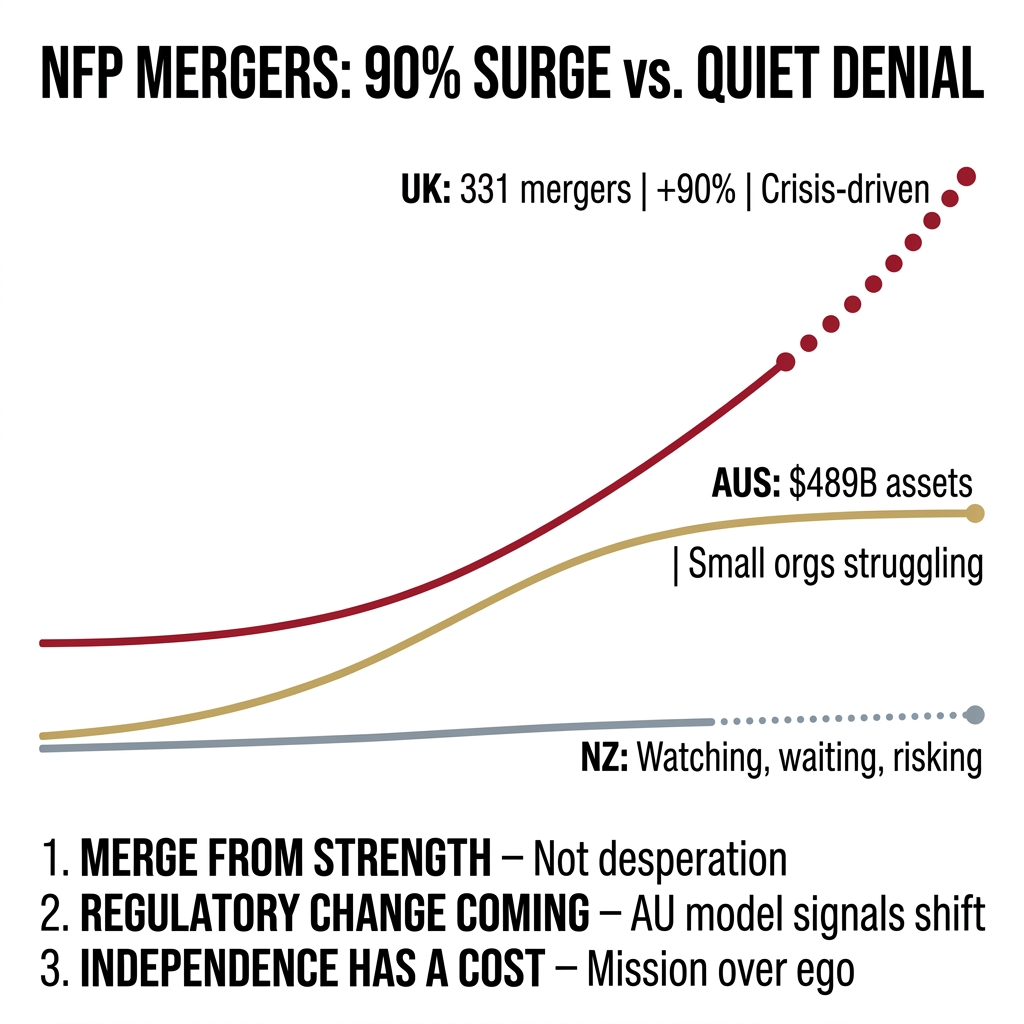

Different data sources track UK charity mergers. RSM UK analysis shows mergers jumped from 174 in 2023 to 331 in 2024 (a 90% increase). Eastside People’s Good Merger Index shows 94 mergers involving 183 organisations in 2024-25, the highest in 12 years. Australia’s charity sector employs 10.7% of the workforce. New Zealand sits between both markets, charting its own course.

I’ve looked at how NFPs in these three countries approach consolidation. The differences matter more than most boards realise.

Why Are UK Charities Merging at Record Rates?

The UK isn’t tiptoeing into merger conversations. They’re being forced into them.

In 2024-25, the sector saw 94 mergers involving 183 organisations. That’s 49% more than the previous year and nearly double 2022-23 figures.

These aren’t strategic choices. They’re survival moves.

Smaller charities face the harshest pressure. In 2024-25, 88 organisations with income under £1 million merged, up from 65 the previous year. The pattern is straightforward: small and struggling means consolidation becomes your only option.

Financial pressure is hitting the entire sector. In 2023, 42.6% of charities reported expenditure exceeding income, up from 38.3% in 2022. These aren’t just small organisations struggling.

The UK also faces fraud problems pushing organisations together. The 2024 Charity Fraud Report found 42% of charities experienced fraud or attempted fraud, with 84% suffering financial loss. Larger charities have stronger cyber security. Smaller ones merge to access those protections.

Key point: The UK model shows what happens when economic pressure becomes relentless. Mergers stop being strategic and start being compulsory. For New Zealand NFPs, what’s happening in the UK today might be our reality tomorrow.

What’s Happening with Australian NFP Mergers?

Australia’s charity sector appears healthy on the surface. Between 2022 and 2023, assets increased by £32 billion to £489 billion. Revenue grew 10.7% to £222 billion. The sector employs more people than construction.

Look underneath though.

About 60% of Australia’s charities operate with revenue below £500,000. Half bring in less than £50,000. These organisations are barely surviving as headline numbers climb.

Expenses increased by £22 billion (up 12.6%). That’s twice the inflation rate. Revenue grows, but costs grow faster.

Small charities face particular vulnerability. 45% of small charity staff were casual, compared with 23% at extra large charities. Job security is a luxury small organisations cannot afford.

Australia is introducing something New Zealand should watch: a mandatory merger notification regime starting 1 January 2026. Charities and not-for-profits aren’t exempt. If your organisation meets certain thresholds, you’ll need to notify the Australian Competition and Consumer Commission before completing a merger.

This changes the equation. M&A in the NFP sector is no longer a quiet handshake between boards. It’s a regulated process with compliance requirements and potential delays.

Key point: Australia shows that sector growth masks individual organisation struggle. Big numbers appear strong, but thousands of small charities are barely surviving. Regulatory changes are coming, adding complexity to an already difficult decision.

Where Does New Zealand Sit on NFP Consolidation?

New Zealand doesn’t have the UK’s dramatic merger surge or Australia’s regulatory overhaul. We’re watching both markets as we deal with our own pressures.

Our NFP sector faces similar challenges: rising costs, static or declining revenue, increased compliance demands, donor fatigue. But we’re not seeing the same consolidation volume.

Why not?

Part of it’s cultural. New Zealand organisations value independence and local identity. Merging feels like losing something, even when the numbers say otherwise. We’re also a smaller market, meaning fewer organisations hit the scale where merger becomes inevitable.

The pressures are building. I’ve worked with NFP boards who know they need to consolidate but struggle to get stakeholders aligned. The conversation stalls because nobody wants to be the one who gave up on the original mission.

The risk is waiting too long. The UK shows what happens when you merge out of desperation rather than strength. You lose negotiating power. You accept terms you wouldn’t have considered five years earlier. You’re combining two struggling organisations instead of two healthy ones.

Key point: New Zealand’s cultural resistance to consolidation creates a dangerous delay. Organisations wait until crisis hits, guaranteeing worse outcomes.

What Really Drives NFP Mergers Across These Three Countries?

After looking at all three markets, patterns emerge that don’t match official narratives.

Financial pressure is the real driver. Organisations talk about increased impact and strategic alignment, but most mergers happen because one or both parties are running out of runway. The UK data proves this: takeovers accounted for 50 out of 63 deals in 2023-24. That’s not collaboration. That’s acquisition.

Smaller organisations merge to access infrastructure. In Australia and the UK, small charities combine to access systems, security, and staff stability they cannot afford alone. It’s not romantic, but it works.

Regulatory complexity accelerates consolidation. Australia’s new merger notification regime will push organisations to think harder before pursuing M&A, but it will also legitimise the process. When government regulates something, it becomes normal business practice.

Donor behaviour matters more than organisations admit. UK data shows 50% of adults donated to charity in the last 12 months, down from 58% in 2019. That’s four million fewer donors. When the donor pool shrinks, organisations compete harder for the same money. Merging becomes a way to reduce competition and increase efficiency.

Key point: NFP mergers are driven by financial survival, infrastructure needs, regulatory pressure, and shrinking donor pools, not the strategic narratives in official communications.

What Questions Should New Zealand NFPs Be Asking About Merger?

I’ve sat in enough boardrooms to know how these conversations go. Someone raises merger. The room goes quiet. Then someone says, but we’ve been serving this community for 40 years.

That’s valid. It’s not a strategy.

New Zealand NFPs need to ask harder questions:

Are we merging from strength or weakness? The strongest mergers happen when both organisations are healthy enough to negotiate as equals. Waiting until you’re desperate limits your options.

What does our community need? Sometimes the answer is two separate organisations. Sometimes it’s one larger, more capable entity. The mission should drive the structure, not the other way around.

Do we have the financial capacity to stay independent? Independence has a cost. If maintaining it means cutting programmes, reducing staff, or compromising service quality, you’re not serving your mission. You’re protecting your structure.

What lessons are available from the UK and Australia? Both markets are ahead of us in the consolidation cycle. Their experiences are available if we’re willing to look.

Key point: The merger conversation needs to shift from protecting legacy to serving mission. Hard questions about financial viability and community need should drive the decision.

How Should NFP Leaders Approach Merger Today?

Start by getting honest about the numbers. Not the budget you present to funders. The real numbers. How long do you sustain operations without significant change? What happens if your largest funder cuts you by 20%? What if you lose your CEO?

Then look at the landscape. Who else does similar work? Where’s the duplication? Where are the gaps? Are you the best organisation to fill those gaps, or would partnership make more sense?

Stop treating merger as failure. In commercial sectors, consolidation is normal. Good companies combine to create better companies. The NFP sector needs the same mindset.

Act whilst you still have options. The UK data is straightforward: organisations that wait until crisis hits get worse outcomes. The time to explore merger is when you’re not desperate for it.

Key point: Proactive assessment of financial reality, competitive landscape, and partnership opportunities creates better merger outcomes than reactive crisis management.

What Will the Next Five Years Look Like for NZ NFPs?

New Zealand will see more NFP mergers. The economic pressures aren’t going away. Government funding is unpredictable. Donors are stretched. Costs keep rising.

The organisations that thrive will make strategic decisions early. They’ll look at the UK and Australia, learn from what’s happening there, and act before crisis forces their hand.

The ones that struggle will wait, hoping things improve. They’ll merge eventually, but from weakness rather than strength.

I’ve seen this pattern play out across sectors for three decades. The NFP world isn’t exempt from economic reality. The sooner boards accept this, the better decisions they’ll make.

If you’re leading an NFP and wondering whether consolidation makes sense, the answer is probably yes. The question is whether you’ll explore it whilst you still have negotiating power, or wait until your options narrow.

The UK and Australia are showing us what’s coming. Learn from them, or repeat their mistakes.

I know which option makes more sense.

Frequently Asked Questions About NFP Mergers

When is the right time for an NFP to consider merger?

Before you need to. Strong mergers happen when both organisations are financially stable and negotiating from strength. Waiting until crisis hits limits your options and worsens outcomes.

How do you know if a merger is right for your organisation?

Ask three questions: Are we financially viable long-term? Does our community need one strong organisation or two separate ones? Does independence serve our mission or our structure? If the answers point towards consolidation, explore it.

What’s the difference between UK, Australian, and NZ NFP mergers?

UK mergers are driven by financial desperation, with a 90% increase in 2024. Australia faces regulatory changes with mandatory merger notifications from 2026. New Zealand has cultural resistance to consolidation despite similar financial pressures.

Do NFP mergers improve service delivery?

When done from strength, yes. Merged organisations access stronger infrastructure, better financial stability, and improved systems. When done from desperation, outcomes are mixed because you’re combining two struggling entities.

How does the new Australian merger notification regime work?

From 1 January 2026, Australian charities meeting certain thresholds must notify the ACCC before completing a merger. This adds compliance requirements and potential delays to the process.

What happens to small charities that don’t merge?

UK and Australian data show small charities face increasing financial pressure, reduced donor support, and limited infrastructure. Many cut programmes or close. Merger becomes necessary to access larger organisation resources for survival.

How do you maintain mission and identity after a merger?

Strong mergers align on mission before discussing structure. Identity concerns are valid, but if maintaining separate identity means cutting services to your community, you’re prioritising structure over purpose.

What mistakes do NFP boards make when considering merger?

Waiting too long, merging from desperation rather than strength, prioritising organisational ego over community need, failing to learn from UK and Australian experiences.

Key Takeaways

-

UK charity mergers jumped 90% in 2024, driven by financial survival rather than strategic choice. Small charities with income under £1 million are being squeezed hardest.

-

Australia’s NFP sector shows strong headline numbers (£489 billion in assets) but 60% of charities operate on less than £500,000 revenue, with costs growing faster than income.

-

New Zealand sits between both markets, with cultural resistance to consolidation creating dangerous delays. Organisations wait until crisis removes negotiating power.

-

Financial pressure, infrastructure access, regulatory changes, and shrinking donor pools drive mergers, not the strategic alignment narratives in official communications.

-

The strongest time to explore a merger is before you desperately need it. Organisations that wait until crisis hits get worse outcomes and limited options.

-

NFP boards need to shift the conversation from protecting legacy structures to serving mission. Hard questions about financial viability should drive decisions.

-

The UK and Australia are ahead of New Zealand in the consolidation cycle. Their lessons are there if boards are willing to look and act.

Leave a comment